CICC: How many more rate cuts will the Fed make?

At the conclusion of the November FOMC meeting today, the Federal Reserve cut interest rates by 25 basis points to 4.5-4.75%, as expected. Powell addressed recent employment and inflation trends, the impact of the US election on future rate cuts, and even the possibility of his resignation, during a press conference [1]. Overall, the meeting maintained a neutral tone, adopting an open-ended approach to future policy. Market reaction was positive, with US Treasury yields and the dollar falling, while the Nasdaq and gold rebounded.

Time:

2024-11-08 15:14

At the conclusion of the November FOMC meeting today, the Federal Reserve cut interest rates by 25bp to 4.5-4.75%, as expected. Powell addressed recent employment and inflation trends, as well as the impact of the US election on the prospects for rate cuts, and even whether he might resign, in a press conference [1]. Overall, the meeting's tone was neutral, with an open attitude towards future paths. The market reacted positively, with US Treasury yields and the dollar falling, while the Nasdaq and gold rebounded.

Since the surprise 50bp rate cut in September ("The Fed's Unconventional Rate Cut Opening"), the Federal Reserve has experienced unexpectedly high inflation (September CPI), two non-farm payrolls that exceeded and fell short of expectations (September and October), and Trump's election victory ("What Does Trump 2.0 Mean for the World?"). Market expectations have also swung from pessimism to optimism: from concerns before the September rate cut that the US was about to fall into recession, to the realization that a recession wasn't imminent and a "soft landing" was possible, to concerns that the Fed's rate cuts were too rapid and that Trump's victory might accelerate the risk of secondary inflation.

With US Treasury yields hitting new highs and Trump's election, the market's main concerns are: why did Treasury yields fall after the Fed's rate cut? How many more rate cuts will the Fed make? How will the US election affect future rate cut prospects?

Q1. What adjustments did the Fed make to its policy and statements? A 25bp rate cut as expected, minor wording adjustments, and a narrowing of the market's rate cut path.

The Fed's 25bp rate cut brought the benchmark rate down to 4.5-4.75%, in line with market expectations. In its statement, the Fed slightly modified its wording on employment and inflation. For example, the description of the job market changed from "slowed" to "generally eased," given that the data from the past two months were significantly affected by temporary factors (such as hurricanes and strikes). The phrase "further" was removed from the description of inflation continuing to decline, and the committee's wording about having greater confidence in inflation returning to 2% was also removed, because September's inflation was unexpectedly high, and the market is concerned that Trump's policies could lead to renewed inflation. It's clear that the Fed's assessment has changed subtly, but it doesn't believe there's a significant risk of deviating from its targets (Powell stated that "the job market is not a major source of inflationary pressure").

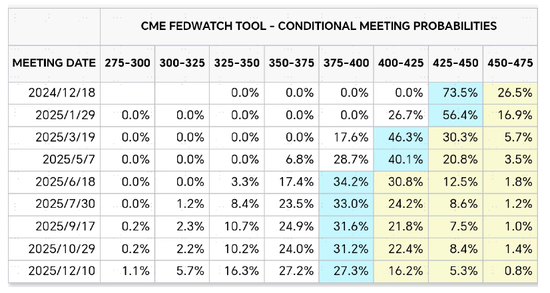

Regarding future rate cut paths, Powell emphasized that decisions will be made based on economic conditions at each meeting (not on any preset course). This is understandable, as the impact of the US election on growth and inflation still needs time to be assessed. Powell said that before the December FOMC meeting, there will be another non-farm payroll report and two inflation reports, which will provide more policy guidance. The implied rate cut path from CME futures has significantly narrowed to a total of three more rate cuts: one each in December of this year, March, and June of next year, with the federal funds rate reaching 3.75-4% by June 2025.

Chart: The implied rate cut path from CME futures has significantly narrowed to a total of three more rate cuts.

Source: CME, CICC Research Department

Q2. Why did Treasury yields rise instead of fall after the rate cut? Correcting pessimistic expectations, interest rate reflexivity, and the "Trump trade".

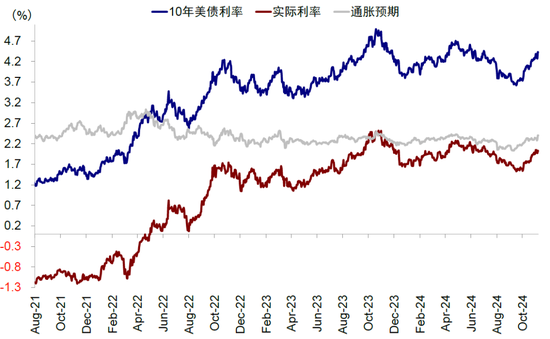

A seemingly strange phenomenon is that after the Fed's rate cut, Treasury yields rose instead of falling, reaching their low point at 3.6% before rising to 4.4%, an increase of 81bp, with inflation expectations rising by 31bp and real interest rates rising by 50bp. This is consistent with our repeated warnings that rate cuts should be "done and thought about in reverse," and that when a rate cut is implemented, it may be the bottom for Treasury yields, mirroring the 2019 rate cut cycle ("Rate Cut Trading Manual").

There are three reasons for this: First, a correction of previously overly pessimistic recessionary expectations. We do not agree with the amplified recessionary concerns driven by sentiment ("Basis for Judging Recessions and Historical Experience"), especially as some data has improved, and market pessimism has been corrected; second, the "reflexivity" of rapidly falling interest rates. The Fed's unconventional rate cuts can actually increase the probability of a "soft landing" by guiding down Treasury yields and all other financing costs based on them, which can re-ignite some demand and improve long-term growth expectations, leading to a rise in Treasury yields. This reflexivity is also at play when interest rates are rising. Third, the boost from the "Trump trade." Trump's improving election prospects, especially his victory, have further pushed up interest rates due to higher growth and inflation expectations ("What Does Trump 2.0 Mean for the World?").

If the third point's expectations are more likely to be emotional speculation with little concrete evidence, the first two are sufficient to support the rise of Treasury yields from their bottom after the rate cut. In other words, the current level may be somewhat overextended, but the upward direction is largely clear. Our estimated reasonable central range is around 3.8-4%, so the previous level of 3.6% for Treasury yields was clearly too low. We will see if the current 4.5% level can be effectively broken through due to sentiment and event factors; otherwise, it will provide trading opportunities.

Chart: The Fed's rate cut became the low point for Treasury yields, rising from 3.6% in September to 4.4%, an increase of 81bp.

Source: Bloomberg, CICC Research Department

Chart: Changes in the US-China credit cycle will determine asset trends.

Source: CICC Research Department

Q3. Will the election affect the Fed's decisions? No in the short term, but inevitably in the long term; the risk of rising interest rates is greater than the risk of falling interest rates.

There is no direct short-term impact, but there will be a long-term impact on growth and inflation. Powell said there is no direct short-term impact, but over time, post-election policies will have economic consequences. This answer is expected. We believe the subtext is that the Fed's rate cut decisions are not political decisions and will not change because of the election results. However, in the long term, many of Trump's policy proposals will inevitably affect future growth and inflation prospects, which will in turn affect the Fed's rate cut decisions.

When asked if he would resign if asked to, Powell said he would not, and also said that Trump could not legally remove him from office. Earlier, Trump also said he was not seeking to remove Powell prematurely, but welcomed a more dovish monetary policy [2]. One of Trump's policies is low interest rates, and during his previous term he publicly criticized Powell's interest rate hikes on multiple occasions [3], which sparked market concerns about the independence of the Federal Reserve. But he also made it clear that "although the two have had disagreements, he will not seek to remove Powell as chairman of the Federal Reserve prematurely". Powell's second term as chairman of the Federal Reserve will last until May 2026, and his 14-year term on the Federal Reserve Board will end in January 2028.

With Trump's election, especially with a "Republican sweep," the upward risk to interest rates is greater than the downward risk. In Trump's policy framework, whether it's the incremental stimulus of tax cuts and increased investment, the supply disruptions of tariffs and immigration, or the less clear but more significant impact of a weaker dollar policy, the impact on interest rates is upward rather than downward. The Tax Foundation predicts that tax cuts for residents and businesses could boost GDP growth by 2.4ppt over the next 10 years [4], but tariffs would suppress GDP growth by 1.7ppt, for a combined boost of 0.8ppt. PIIE estimates that CPI could rise by 4-7ppt in the next 1-2 years under a baseline scenario of 1.9% due to tariffs [5]. The recent surge in US Treasury yields, especially the sharp rise to 4.4% on election day, reflects the impact of his policies.

Q4, how many more rate cuts? Around 3.5% is an appropriate level; the market has swung from overly optimistic to overly pessimistic.

Market expectations for future rate cuts have swung from one extreme to the other recently, influenced by recent economic data and especially post-election expectations. Currently, CME interest rate futures expect only 3 more rate cuts, in December this year, March and June next year, with the terminal rate at 3.75-4%. While we have never agreed with the previous overly optimistic market view that assumed consecutive 50bp rate cuts, leading to more than 200bp of rate cuts next year, the current expectation may be overly pessimistic. Our comprehensive calculations suggest that a rate cut of around 3.5% (i.e., another 100bp rate cut) would be an appropriate level.

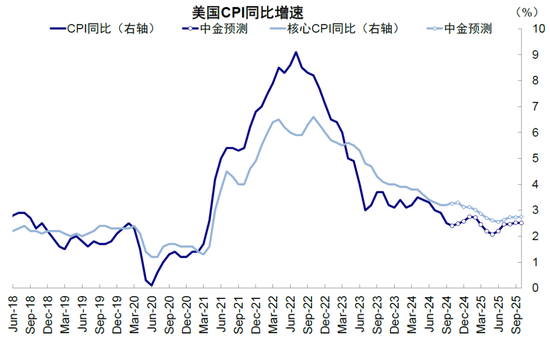

► In terms of pace, inflation and economic data may gradually pick up in mid-2025, leading to a gradual halt in rate cuts. Our calculations show that inflation will tail off in the fourth quarter of this year due to base effects, but with the downward pressure from rents, inflation and core inflation are unlikely to fall significantly until the first quarter of 2025. Our calculations show that by mid-2025, the largest component of CPI, rent, may turn upward again, and with the recovery of demand, the upward pressure on other components will also be greater, with CPI year-on-year in 2025 above 2%, around 2.5% in 3Q25. The risk of upward inflation is greater than the risk of downward inflation, with risks stemming from an earlier recovery in demand and current supply chain disruptions, such as the situation in the Middle East, port strikes, and potential trade friction and immigration restrictions.

Chart: With Trump's election, especially with a "Republican sweep," the upward risk to interest rates is greater than the downward risk.

Source: CICC Research Department

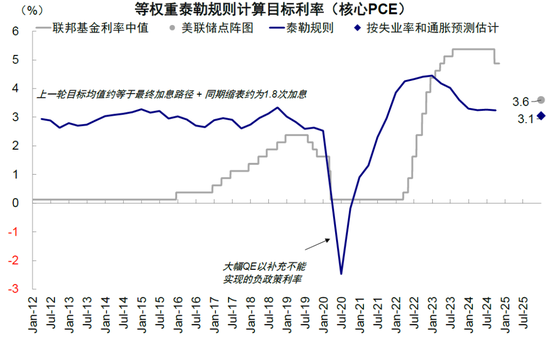

► In terms of magnitude, a rate cut to around 3.5% is a reasonable level. 1) Return monetary policy to a neutral perspective: Referring to the average of the Federal Reserve model and dot plot estimates of the natural interest rate, the actual natural interest rate in the United States is around 1.4%. Considering that short-term PCE may be around 2.1%~2.3%, a rate cut of 4~5 times 25bp to 3.5%~3.8% is a reasonable level. 2) Taylor rule perspective: Assuming that the Federal Reserve in 2025 gives equal weight to achieving inflation and employment targets, its long-term inflation and unemployment rate targets are 2% and 4.2%, respectively, and the long-term estimate for the federal funds rate is 2.9%. Based on our estimates of the year-end unemployment rate and inflation rate of 4.2% and 2.3% (core PCE year-on-year), the appropriate federal funds rate under the equal-weighted Taylor rule is 3.1%, but the tail-off and risks of year-end inflation may lead to a smaller rate cut.

Chart: CPI year-on-year in 2025 is above 2%, around 2.5% in 3Q25.

Source: Haver, CICC Research Department

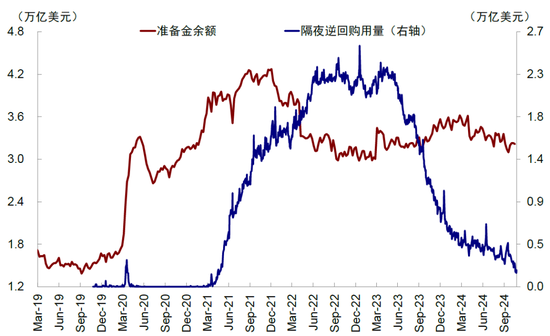

Q5, when will the balance sheet reduction stop? Continuously tightening financial liquidity may prompt the Federal Reserve to gradually exit balance sheet reduction soon.

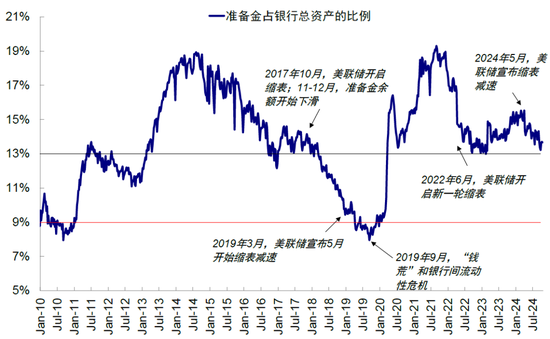

The main basis for the pace of balance sheet reduction is whether reserves are sufficient. The sufficiency of reserves is subject to non-linear changes ("How will the Federal Reserve end balance sheet reduction?"), so close monitoring and early prevention are crucial. To a certain extent, in 2019, the Federal Reserve misjudged the impact of balance sheet reduction and the scale of reserves needed by the financial system, leading to a "cash crunch" in the repo market, and ultimately being forced to expand its balance sheet. This precedent provided ample reason for the slowdown in the pace of balance sheet reduction in May this year. The New York Fed's July survey of major US banks [6] shows that most banks expect quantitative tightening to end in April next year.

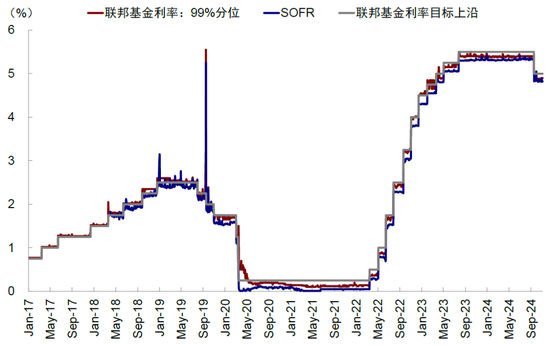

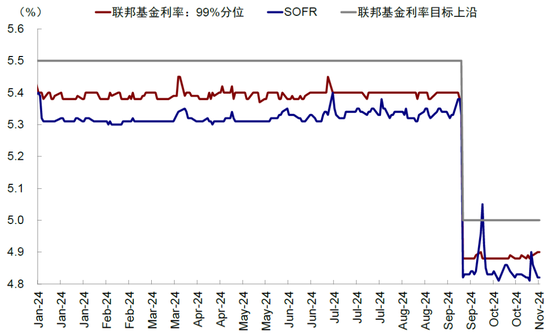

Stopping balance sheet reduction or gradually entering the field of vision. 1) Overnight reverse repurchase agreement balances are no longer abundant: According to Federal Reserve data, overnight reverse repurchase agreements, which once reached over $2 trillion, are a symbol of abundant liquidity in the United States and effectively offset the impact of the Federal Reserve's balance sheet reduction. However, this amount has now fallen to less than $200 billion. 2) Reserves/bank assets are approaching the critical value: The reserve demand curve is non-linear. Measured by the ratio of reserves to bank assets, 12%~13% is the critical point between excessive and moderate sufficiency, while 8%~10% is the warning line for a shortage [7]. This value has now fallen to 13.7%, and from the 2019 experience, the possibility of future non-linear changes is increasing. 3) Liquidity indicators are tightening: Unsecured rates such as the federal funds rate and secured rates such as SOFR are important observation indicators in the interbank market. When liquidity in the interbank market is tight, the rate at which reserves are lent at the highest premium (99th percentile federal funds rate) will be very close to or even exceed the upper bound of the target range, and SOFR will also surge significantly. During the 2019 "cash crunch," these two rates broke through the Federal Reserve's set upper bound of 2.25% for the federal funds rate at 5.55% and 5.25%, respectively. In October this year, SOFR broke through the upper bound again, causing widespread concern.

Chart: The appropriate federal funds rate under the equal-weighted Taylor rule is 3.1%, but the tail-off and risks of year-end inflation may lead to a smaller rate cut.

Source: Haver, Federal Reserve, Bloomberg, CICC Research Department

Chart: Overnight reverse repurchase agreement balances are no longer abundant.

Source: Haver, CICC Research Department

Chart: Reserves/bank assets are approaching the critical value.

Source: Wind, Haver, CICC Research Department

Chart: During the 2019 "cash crunch," these two rates broke through the Federal Reserve's set upper bound of 2.25% for the federal funds rate at 5.55% and 5.25%, respectively.

Source: FRED, CICC Research Department

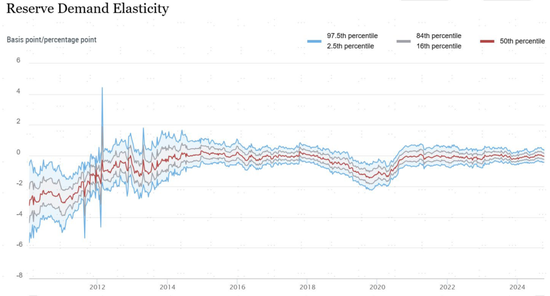

It is precisely because of these changes that the market and the Federal Reserve have begun to discuss liquidity and balance sheet reduction more frequently. In October, the Federal Reserve released a new observation tool—the Reserve Demand Elasticity Index (RDE). The lower the value of this index, the greater the impact of reserve changes on interest rate fluctuations, and the more scarce the reserves. As of October data, the index is close to 0 (usually in the negative to 0 range), indicating that reserves are still ample. Overall, a severe liquidity shock is unlikely in the short term, but it is getting closer and closer to the threshold for stopping balance sheet reduction, and stopping balance sheet reduction also means a full easing of monetary policy.

Chart: SOFR broke above the upper bound again in October this year.

Source: FRED, CICC Research Department

Q6. What is the impact on assets? Short-term election trading dominates, providing trading opportunities after a surge.

As we analyzed in (What does Trump 2.0 mean for the world?), a Trump victory, especially a "Republican sweep," would provide momentum for related assets to surge, benefiting risky assets and dollar assets. However, considering that expectations are factored in and policies take time to implement, the surge will also provide some "contrarian" trading opportunities, such as US Treasury yields. 1) Overall, Trump trades have further room to surge and play out; "let the bullets fly a little longer"; 2) For assets with less or no factored-in expectations of Trump's policies, such as copper, oil, and export chains, if subsequent policies are implemented, the degree of compensation needed will be greater; 3) After surging to a certain extent, such as US Treasuries and the dollar, contrarian trading opportunities will be provided. Gold has excessive factored-in expectations and is contrary to the direction of increased risk appetite, therefore there is a risk of overspending, as was the case in the two previous elections in 2016 and 2020. We have consistently pointed out that the beginning of rate cuts is also the end of rate cut trades. Looking back, the September Fed's 50bp "unconventional rate cut" opening actually created a bottom for interest rates, this seemingly "divergent" trend is consistent with the "think contrarian, act contrarian" approach we have repeatedly emphasized in our reports.

In the medium term, the election will bring significant changes to the outlook for US domestic growth and inflation, as well as China's response to external and domestic demand, but a moderate restart of the US credit cycle and a no longer shrinking Chinese credit cycle remain the baseline scenario, at which point US assets are still not bad, and China still focuses on structure.

Chart: The reserve demand elasticity index constructed by the Federal Reserve is close to 0, indicating that reserves are still ample.

Source: Federal Reserve Bank of New York, CICC Research Department

► US equities are unlikely to perform poorly, with technology and cyclical sectors as the main themes. Short-term valuations are high, and policy uncertainties will bring disturbances, but the long-term growth outlook is not bad, driven by technological trends and the cyclical sectors after the natural restart of the private credit cycle, which is also the main allocation theme, so dips are also opportunities for allocation.

► US Treasuries are likely to perform poorly, but there are trading opportunities. We have consistently pointed out that the realization of rate cuts may be the low point for long-term US Treasury yields, and the yield curve is flattening, which is indeed the case. Looking ahead, the low point of interest rates has passed, but due to short-term overspending, trading opportunities will still be provided.

► The US dollar is strong, but we need to pay attention to intervention policies. The natural recovery of the US economy and incremental policies after the election will support the US dollar, and our estimated central tendency is 102-106. However, more importantly, Trump and his key economic advisor Lighthizer have repeatedly proposed the view of competitive devaluation of the dollar.

► Commodities are neutral to bullish. Copper demand is more related to China, while oil is more affected by geopolitics and supply. From the perspective of the US-China credit cycle, we believe that it is not meaningful to be further bearish at the current level, but the upward momentum and time are still unclear and need to wait for catalysts.

► Gold is neutral. Gold has already exceeded the 2400-2600 USD/oz level that our fundamental quantitative model based on real interest rates and the US dollar index can support. However, geopolitical situations, central bank gold purchases, and local "de-dollarization" demand have brought additional risk premium compensation. We estimate that since the Russia-Ukraine conflict, the average has been 100-200 USD. It can still be used as uncertainty hedging in the long term, but we recommend a neutral stance in the short term.

Related News

Gold prices continue to fluctuate.

Gold prices have shown a volatile pattern in the short term, affected by the weakening of the US dollar and changes in sentiment due to easing geopolitical tensions.

Gold prices rise again! Multiple risks fuel safe-haven demand.

From the perspective of the international market, the tense situation in the Middle East, the escalation of the Russia-Ukraine conflict, and the continued high uncertainty surrounding the US Trump administration's tariff policies have driven up gold prices due to increased risk aversion in the market. Furthermore, a significant recent change in the gold market is that gold has become the second-largest reserve asset for central banks globally. How should the future trend of gold prices be viewed? Several analysts have indicated that in the short term, gold prices may fluctuate due to factors such as tariff easing and sudden changes in the geopolitical situation; in the medium to long term, gold prices are still in an upward channel.

As the Russia-Ukraine conflict enters its third year, global attention is once again focused on this geopolitical crisis. According to Dow Jones Newswires, US President Donald Trump made startling remarks at the White House on Thursday (June 5), stating that neither Russia nor Ukraine is prepared for peace, and that both sides may "continue fighting" until one side is willing to compromise. This statement not only signals the failure of his attempts to broker peace, but also introduces new uncertainty to the global geopolitical and economic markets.

Recently, good news came from the China Machinery Metallurgy and Building Materials Workers' Technical Association. In the 2025 National Machinery Metallurgy and Building Materials Industry Workers' Technological Innovation Achievement Award, Shandong Guoda Gold Co., Ltd.'s "Purification of Crude Arsenic Flue Dust to Produce Arsenic Trioxide Industrial Application" and "Key Technology Application for High-Value Utilization of Complex Copper-Gold Ore Resources" projects won the first prize and the second prize respectively. This honor is a high recognition of the workers' technological innovation ability and the effectiveness of achievement transformation, and also fully demonstrates the company's outstanding strength in the industry.

Gold prices return to $3300! Wall Street banks show significant divergence in long-term outlook

In fact, as gold prices fluctuate, Wall Street's major banks have recently shown a clear divergence in their views on gold prices. Unlike Goldman Sachs and Deutsche Bank, which are optimistic about gold's performance, Citigroup believes that the long-term outlook for gold prices is not optimistic.

Although gold prices rose this week, market volatility has clearly increased. While the US-UK agreement is symbolic, its content is limited and insufficient to alleviate concerns about a global economic slowdown. Therefore, gold prices will continue to fluctuate between safe havens and policy signals, closely monitoring the Federal Reserve's interest rate expectations and global trade sentiment.